First-time homebuyers are back but paying through the nose

Even as home prices drop, housing affordability remains a challenge for many first-time buyers

Buyers are willing to pay: First-time home purchases rise in 2022

FOX Business' Jeff Flock discusses how first-time house buyers are navigating the housing market amid fears of rising interest rates on 'Varney & Co.'

As the housing market begins to cool, first-time home buyers are coming back after years of setbacks.

First-time home buyers now represent 45% of all buyers, up from 37% of buyers surveyed last year and rebounding to pre-pandemic levels, according to Zillow’s 2022 Consumer Housing Trends Report. In 2018, first-time buyers made up 46% of the share of all buyers.

Part of the reason that the share of first-time shoppers is rising is because fewer repeat buyers are pulling out of the market. As interest rates continue to rise, existing homeowners who locked in a low rate or refinanced a home over the past few years are staying put. That is boosting favor to new buyers who have been outbid consistently for two years by repeat buyers strapped with cash and equity from previous homes.

MORTGAGE RATES DOUBLE VS. YEAR AGO, REFINANCINGS HIT 22-YEAR LOW: SURVEY

"It’s less competitive now," Dominique Dredden, a first-time homebuyer in Philadelphia, told FOX Business. "A year ago, going to open houses was like going to fall festival. Everybody was looking at the same house. That’s not the case now."

Dredden decided to buy a home last month to hedge against rising mortgage rates. She began her search several years ago and pulled out when 15 people started showing up to house showings at a time around a year ago. Home inspectors and appraisers, bombarded with requests, were also unavailable at the time.

Dredden made the jump once prices began to decline over the last several months and the mortgage rates began to climb. The 30-year fixed-rate mortgage averaged 6.92% in the week ending Oct. 13, according to Freddie Mac. That figure is up from 3.05% a year ago and the highest average rate recorded since April 2002.

First-time homeowners may also have more bargaining power as a number of sellers drop their prices and more homes become available for sale in the market.

HOW HOUSING IS FUELING RED-HOT INFLATION

Price growth is softening on a monthly level nationwide and in many markets across the country, with the largest monthly drop in home values, 0.3%, since 2011. Even as home prices drop, housing affordability still remains a challenge for many first-time buyers.

"The interest rates that have continued to rise over the past several months have really outweighed any of the small drops in home prices that we've seen in the last couple of months," Nicole Bachaud, senior economist at Zillow, told FOX Business. "That's really leading to housing remaining unaffordable, and it's not going to really get better anytime soon. Affordability is still going to be a big challenge."

HOMEBUILDERS SEE 'HOUSING RECESSION' AS SENTIMENT PLUNGES TO FRESH 2-YEAR LOW

While appreciation has receded since peak prices in April, the typical home values are still up 14.1% from a year ago and 43.8% since August 2019, according to Zillow. Interest rates are expected to remain high, and home prices are unlikely to dip back to pre-pandemic levels.

With mortgage rates nearing 7%, financing the purchase of a $500,000 home would cost around $3,327 per month as part of a 20% down payment, up from $1,976 per month last year when rates hovered around 2.5%.

GET FOX BUSINESS ON THE GO BY CLICKING HERE

During the pandemic, the share of first-time home buyers dropped as home values skyrocketed and competition remained strong from high demand. Younger, millennial buyers continued to lose out to older, repeat shoppers who could deploy financial leverage from equity in their existing homes and dole out all-cash offers. According to a Zillow survey, 45% of Gen Z and 38% of millennial buyers lost to an all-cash buyer at least once.

Even as affordability continues to be a challenge, people like Dredden say that becoming a homeowner will be more affordable than alternative housing options like renting- and that it’s better to get in now before it’s too late.

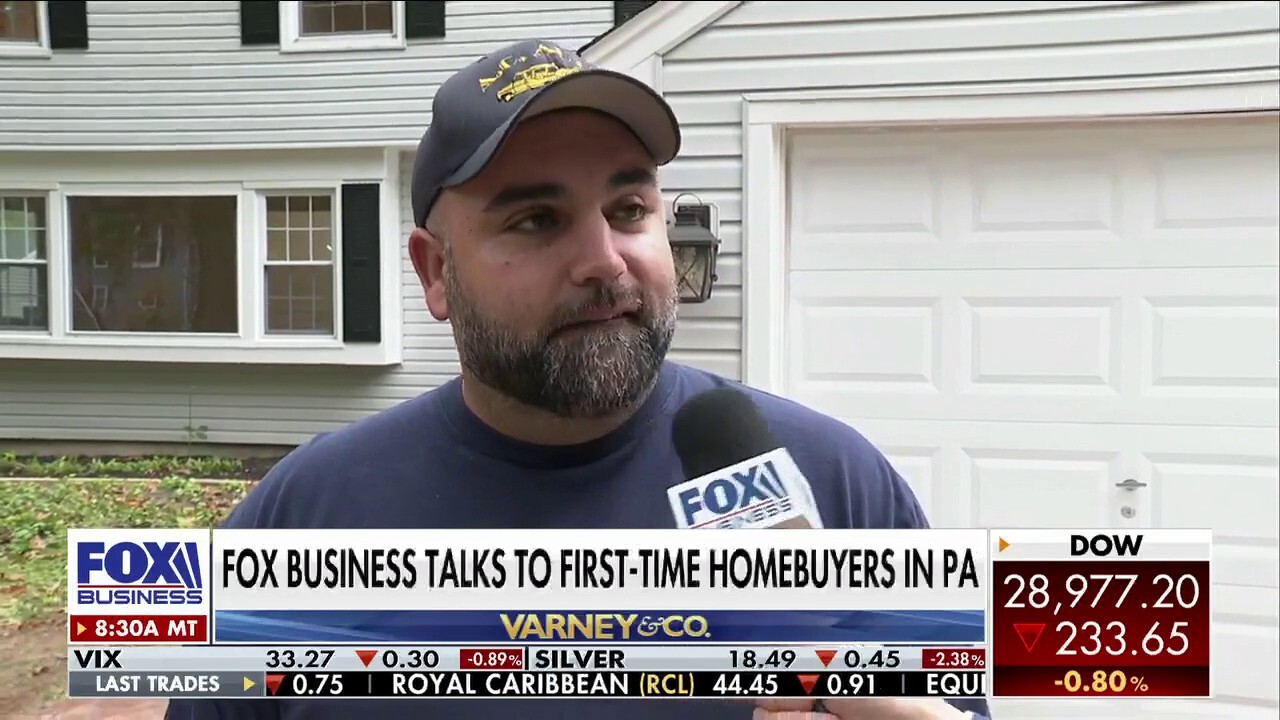

"I feel like now's the time," Nicholas Campione, Philadelphia resident and first-time home buyer told FOX Business. "If I wait, I feel like I'm afraid the interest rates are going to go up."

Campione dropped out of the house hunt just before the pandemic broke out and after being outbid on multiple occasions. As a self-employed mechanic and new father, he said that now is the time to buy even though interest rates and home prices are still high. Now that the bidding competition has somewhat eased, he has more time and flexibility to look at several houses and even turn options down.

Campione is not alone in the pursuit of homeownership as rates are expected to close in on 7% and amid fears of a future recession.

"Yes, the interest rates are going up and the housing market is a little bit more than what it was pre-pandemic, but you have to also consider that renting is even more than a mortgage," Dredden said. "It's going to get high. It's going to get hard. We want to get on top of it now."