3 Top Gold Stocks That Can Be Bought Cheap

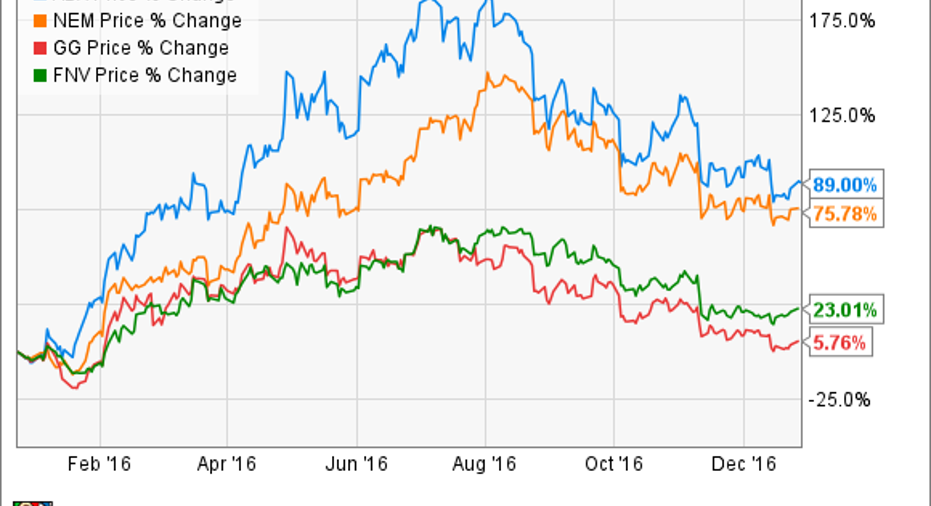

After rallying to a high of $1,365 an ounce this summer, gold has retraced most of its ascent and now stands just 7% above where it started the year. With it have gone some of the biggest names in the industry, though their stock values stand appreciably higher than where they were a year ago. Barrick Gold has nearly doubled in value, Newmont Mining is up 75% for the year, and streamer Franco Nevada gained nearly 25%:

Running with a winner is often a good strategy, but there are three more gold stocks investors should consider for their portfolios not only because they can be bought cheap, but also for the potential they still hold for outsized returns.

Situated for the coming recovery

Unlike its peers, gold-mining giant Goldcorp (NYSE: GG) has had a lackluster year at best, sitting just 10% or so above the year's starting point. Yet the miner has several things going for it that differentiate it from the others, such as having most of its top-producing mines in countries that are relatively politically stable.

The company's principal properties include its top-producing Penasquito gold mine in Mexico; its second-most-valuable project, Cerro Negro, in Argentina, as well as the Alumbrera mine; its gold mines at Red Lake, Eleonore, Porcupine, and Musselwhite in Canada; and the Pueblo Viejo mine in the Dominican Republic.

Inside the Eureka vein at Goldcorp's Cerro Negro mine in Argentina. Image source: Goldcorp.

Goldcorp recently resumed normal operations at Penasquito; it anticipates producing between 520,000 and 580,000 ounces of gold this year, or about 19% of total planned production of between 2.8 million and 3.1 million ounces of gold, which it estimates will have all-in sustaining costs (ASIC) of between $850 and $925 per ounce. Having reduced its ASIC from $1,067 in the second quarter to $812 in the third, Goldcorp sits some 36% below its 52-week high; buying in now positions an investor for the rebound expected to come in 2017.

Standing in the stream

A better way than buying a miner like Goldcorp might be to invest in a company that doesn't get its hands at all dirty digging in the rocks. Instead, streamers like Franco Nevada have become popular because they provide little of the risk or cost associated with owning and operating a mine. Rather, they provide up-front financing to the miners in exchange for receiving a percentage of their production as a royalty, or a stream of precious metals at discounted prices. Their low overhead costs ensure healthy profit margins and the ability to weather industry downturns.

Sandstorm Gold (NYSEMKT: SAND) has outperformed the precious metal itself over the past year, with shares rising 35% year to date. Last month it reported third-quarter profits of $7 million, a big U-turn from 2015, when it suffered losses of $5.5 million. In fact, its entire operation was doing better with greater production: lower cash costs, but higher cash margins; and greater operating cash flows, all of which allowed it to pay down its revolving credit facility. That means it has no bank debt and its entire $110 million revolving credit facility is available to make acquisitions.

Image source: Getty Images.

Taking into account its existing royalties and streams, Sandstorm forecasts attributable gold-equivalent production for 2016 of between 47,000 and 50,000 ounces, hitting 65,000 ounces a year by 2020.

Throwing a curveball

Silver Wheaton (NYSE: SLW), of course, is a streamer like Sandstorm and Franco, but it is the largest in the precious-metals industry, and arguably the best-known, because its business model came to define what streaming is. Although it is known primarily for its silver contracts, Silver Wheaton also has sizable gold production that makes it worth your attention.

As the largest pure precious-metals streamer in the world, Silver Wheaton expects to produce an equivalent of 54 million ounces of silver and 265,000 ounces of gold this year, with gross margins that hit $946 an ounce for gold and more than $15 an ounce for silver during the third quarter. Moreover, for this production, it only has to pay $4.52 per ounce for silver and $403 per ounce for gold.

Image source: Getty Images.

Those kinds of numbersmake Silver Wheaton's future look bright. Yet even though its stock is 45% higher this year, it took a hit in November after reporting third-quarter earnings: The company had record quarterly gold production of more than 109,000 ounces, but changed guidance so that silver production for the year would be less than expected.

What held back the streamer's numbers some was lower production out of Goldcorp's Penasquito mine, but with that now back on track, Silver Wheaton should find itself better positioned even if some of its silver projects lag. And with its dividend for the quarter now increased by 20% to $0.06 per share, investors will be paid a richer reward waiting for the rebound to occur.

10 stocks we like better than Goldcorp When investing geniuses David and Tom Gardner have a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

David and Tom just revealed what they believe are the 10 best stocks for investors to buy right now... and Goldcorp wasn't one of them! That's right -- they think these 10 stocks are even better buys.

Click here to learn about these picks!

*Stock Advisor returns as of Nov. 7, 2016

Rich Duprey has no position in any stocks mentioned. The Motley Fool owns shares of Silver Wheaton. The Motley Fool has a disclosure policy.