File and Suspend: Is This Your Last Chance?

April 30thwill be your last day to take advantage of this Social Security loophole.

Social Security is massively important to America's retirees. According to a reportby the Social Security Administration, over half of married elderly persons -- and nearly three-quarters of elderly single filers -- depend on the program for over half of their income in retirement.

That's a massively important data point that shouldn't be taken lightly. It also underscores how important a perfectly legal loophole that allows married couples to boost their Social Security income has been. That loophole -- referred to as "File and Suspend" -- will be closing on April 30th...likely forever.

Here are the basic facts you need to know.

How benefits are calculated To understand how this loophole works, and whether or not you should consider taking advantage of this closing window -- there are a couple of key pieces of information to know.

- The higher earner of a married couple has his/her benefits calculated based on the 35 highest-earnings years in his/her career. Benefits can be taken starting at age 62, and ending at age 70. For each year a retiree waits to claim benefits, the monthly benefit increases 8%.

- The lower earner of a married couple has two choices. They can either receive their own benefits under the same guidelines as above (if they worked), or they can receive half of their partner's monthly benefits -- referred to as "spousal benefits."

But here's the catch -- and this is the key-- regular retired worker benefits increase by 8% for every year you wait under age 70. But spousal benefits stop increasing once the wage-earner reaches the full retirement age -- which is currently 66.

How file and suspend worksOver time, a number of savvy retirement planners have realized that this discrepancy opened up a loophole. Here's how it worked.

- The wage earner, once he/she reaches 66, files for Social Security benefits.

- The spouse immediately follows for spousal benefits -- and begins receiving those benefits.

- Once step 2 is finished, the wage earner immediately suspends his/her payments, allowing them to grow unabated until age 70.

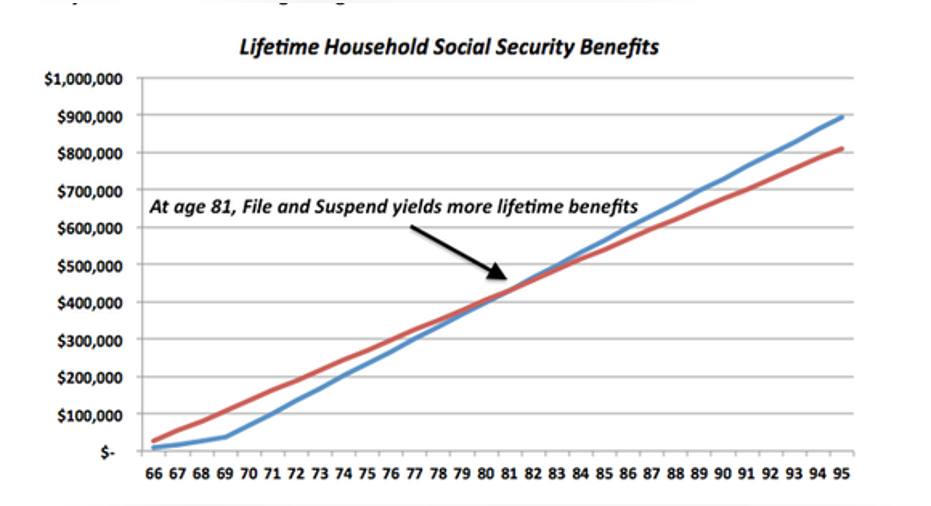

In a previous article on the topic, I used this chart to demonstrate how -- if a couple lives long enough -- it can prove to be a significant boost in lifetime Social Security income. This assumes the wage earner would have benefits of $1,500 per month at age 66.

Source: Author's calculations.

Why it's closingWhen Congress passed its bipartisan budget deal in 2015, a number of loopholes in Social Security were closed. File-and-suspend was one of them. Luckily for those who still want to use the strategy, there's was a 150-day window that was granted before the loophole closes forever. That window will close -- likely forever -- on April 30th.

If this sounds appealing to you, talking to your financial planner ASAP is of the utmost importance. Otherwise, both members of the couple will either have to (1) start receiving benefits at 66, or (2) wait until age 70.

The article File and Suspend: Is This Your Last Chance? originally appeared on Fool.com.

Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright 1995 - 2016 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.