Here's Why Medicare Is in Much More Trouble Than Social Security

It's no secret that two of the most popular federal programs for retirees aren't in great financial shape. Both Medicare and Social Security face significant challenges in the years ahead. But Medicare is in much more trouble than Social Security. Here's why.

Image source: Getty Images

Race to the bottom

When Medicare's trustees reported on the status of the federal healthcare program in 2015, they projected that the Medicare Part A hospital insurance trust fund would run out of money in 2030. Now the trustees estimate that the trust fund will be depleted in 2028 -- two years earlier than previously expected.

Image source: 2016 annual report of the boards of trustees of the Federal Hospital Insurance and Federal Supplemental Medical Insurance Trust Funds.

What about Social Security? There are two parts of the program: Old-Age and Survivors Insurance (OASI) and Disability Insurance (DI). The Social Security trustees project that the DI trust fund reserves will run out of money in 2023, while the OASI trust fund reserves will last through 2035. If the two trust funds are combined, Social Security's trust fund will be broke in 2034 -- six years after Medicare runs out of cash.

The depletion of reserves doesn't mean Medicare will quit paying for retirees' medical bills and Social Security will halt sending checks, however. Even when its trust fund runs out of money, Medicare could still cover 87% of benefits from ongoing funds, including taxes and premiums. Social Security would still be able to pay 79% of scheduled benefits when its trust fund is depleted in 2034.

Medicare's big problem

There's a simple reason Medicare is in worse shape than Social Security. While Social Security benefits are tied to wage growth, Medicare spending is linked to healthcare costs. And healthcare costs are projected to skyrocket, presenting a huge problem for Medicare in years to come.

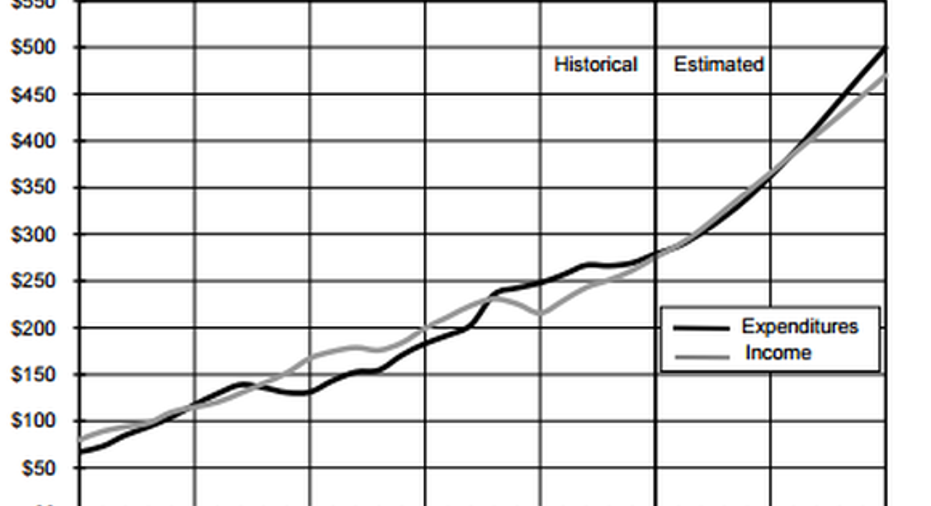

Image source: 2016 annual report of the boards of trustees of the Federal Hospital Insurance and Federal Supplemental Medical Insurance Trust Funds.

Note the steeper upward trajectory of Medicare hospital insurance expenditures beginning after this year. Increased spending in all areas is projected because of the aging U.S. population, with especially high percentage growth inskilled nursing, home health, and hospice costs.

These soaring costs don't include prescription drugs that are part of the Medicare Part D program. The latest projections are that Medicare Part D spending will more than double between 2016 and 2025.

What can be done?

Medicare's actual spending is very difficult to accurately predict because of the variables involved in projecting healthcare costs. However, it's clear that the program is headed in the wrong financial direction. What can be done to avoid a catastrophe?

One option is to increase the amount of revenue coming into Medicare. The most obvious way to do so is a tax increase. The primary source of Medicare Part A funding is the payroll tax. Employers and employees each pay 1.45% of employee wages currently, while self-employed individuals pay 2.9% of net earnings.

Additional revenue could be generated even without a tax increase, though. If more jobs were created, overall tax receipts would increase at current payroll tax rates. Higher-paying new jobs would help the most.

The other primary option is to reduce the rate of growth of Medicare spending. Some hope that efforts to implement value-based payment approaches instead of fee-for-service reimbursement will help accomplish this goal. Others think that implementing a premium support model, where the government provides payments to individuals to purchase health insurance from a private plan or through traditional Medicare, could be the best answer.

Regardless of what steps are ultimately taken, it's clear that something needs to be done. And, as the Medicare trustees said in their report, action needs to be taken "sooner rather than later to minimize the impact on beneficiaries, providers, and taxpayers."

The $15,834 Social Security bonus most retirees completely overlook If you're like most Americans, you're a few years (or more) behind on your retirement savings. But a handful of little-known "Social Security secrets" could help ensure a boost in your retirement income. For example: one easy trick could pay you as much as $15,834 more... each year! Once you learn how to maximize your Social Security benefits, we think you could retire confidently with the peace of mind we're all after.Simply click here to discover how to learn more about these strategies.

Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.