Is Now a Golden Opportunity to Buy Barrick Gold?

Image source: Getty Images.

Barrick Gold (NYSE: ABX), with an improving balance sheet and free cash flow, is an industry leader among gold-mining stocks, and certainly warrants consideration in the gold-mining industry. Now may be a good time to pick up shares. Let's take a closer look, paying particular attention to the company's debt -- a significant concern for any gold-mining stock.

Delving into debt

A company that carries a lot of debt on its balance sheet shouldn't immediately disqualify it from occupying a part of your portfolio. The debt-to-equity ratio is one of several metrics used to gauge a company's leverage. The ratio, gives a sense of how reliant the company is on debt to finance its assets relative to shareholders' equity.

ABX Debt to Equity Ratio (Annual) data by YCharts

Barrick's debt-to-equity ratio has not improved considering the company's $4.1 billion investment over the past six quarters. Compared to its peers, Goldcorp (NYSE: GG), Kinross Gold (NYSE: KGC), and Newmont Mining Corp. (NYSE: NEM), Barrick Gold -- with 40% more debt than shareholder value -- is accepting considerably more risk. Since the company is clearly reducing its debt load, it must be the stockholders' equity that possesses the problem.

ABX Shareholders Equity (Annual) data by YCharts

Barrick Gold's problem is that the value of its assets -- namely, mines -- has plummeted over the past five years. In fact, the company has taken about $27 billion in goodwill and asset impairment charges since 2012. Consequently, the stockholders' equity has also fallen. This would be somewhat tolerable if Barrick Gold's decline was on par with its peers, but that's not the case. Barrick has suffered the steepest decline in shareholders' equity, and even though Kinross Gold (NYSE: KGC) has recognized a similar drop in equity, its debt-to-equity ratio -- at .509 -- remains at a very conservative level.

Looking at liquidity

It seems as though debt is still a serious concern for the company. Although it would be helpful to further evaluate the debt by looking at the company's net debt to EBITDA ratio, which gauges its ability to generate operational profits that support payment of its debt load, this would be futile. According to Morningstar, Barrick Gold last reported positive EBITDA in 2012.

Instead, let's consider another perspective -- liquidity. Although Barrick Gold is aggressively taking on risk, this could be palatable if it is well-suited to service its debt.

We'll use two metrics to gauge its liquidity: the quick ratio and the current ratio. Measuring the company's ability to meet its short-term obligations, the quick ratio subtracts the company's inventories from its most liquid assets -- like cash and short-term investments -- and divides it by its current liabilities. The current ratio, on the other hand, adds inventories back into the equation in order to assess the company's ability to meet short-term and long-term obligations.

ABX Quick Ratio (Annual) data by YCharts

For both metrics, most investors consider a quick ratio above 1.0 as a healthy sign, for it indicates that a company has more than $1 in current assets minus accounts receivable for each $1 of payments due within a year like accounts payable and the current portion of long term debt. Here, we find that Barrick Gold can safely meet both its short-term and long-term obligations. And comparing the company against its peers -- always a prudent step to take -- confirms that Barrick Gold is well-positioned.

Is Barrick a bargain?

At this point, there seems to be nothing remarkable -- either positive or negative -- about Barrick Gold. How about the stock itself? Well, it has certainly been on a good run -- shares are up more than 130% year to date and up more than 180% from this point last year.Let's see if there's still a good value to be had.

Because Barrick Gold hasn't reported positive net income since 2011, the traditional price-to-earnings ratio isn't of much use. Instead, let's value the company from a sales perspective. To do this, we'll use two metrics: free cash flow to sales (FCF/S) and the price-to-sales (P/S) ratio.

To start, we'll apply the FCF/S metric to the companies. This indicates how well a company is able to convert revenue into actual cash. Because earnings figures are susceptible to manipulation by management, many investors place greater emphasis on a company's free cash flow. Afterward, we'll measure this figure against how much the market is willing to pay for each company's sales.

Based on this framework, we're looking for a company that has a high FCF/S percentage and a low P/S -- a company efficient at converting sales to cash and that's not too richly valued. Free cash flow and sales are on a trailing-twelve-month basis.

Data source: Morningstar.

Converting sales into cold, hard cash is in Barrick Gold's wheelhouse -- an area where it greatly outperforms its peers. One would suspect that this demands a premium valuation, however, that's not what we find. Instead, Barrick Gold, trading at 2.5 times trailing sales appears to be attractively priced. Ironically, it's Goldcorp, the least successful at converting sales to free cash flow, which trades at the highest multiple.

This, alone, doesn't suggest that Barrick Gold's shares are a steal. We'll turn to the company's book value -- its total assets minus its total liabilities -- for another perspective on how the stock is priced.

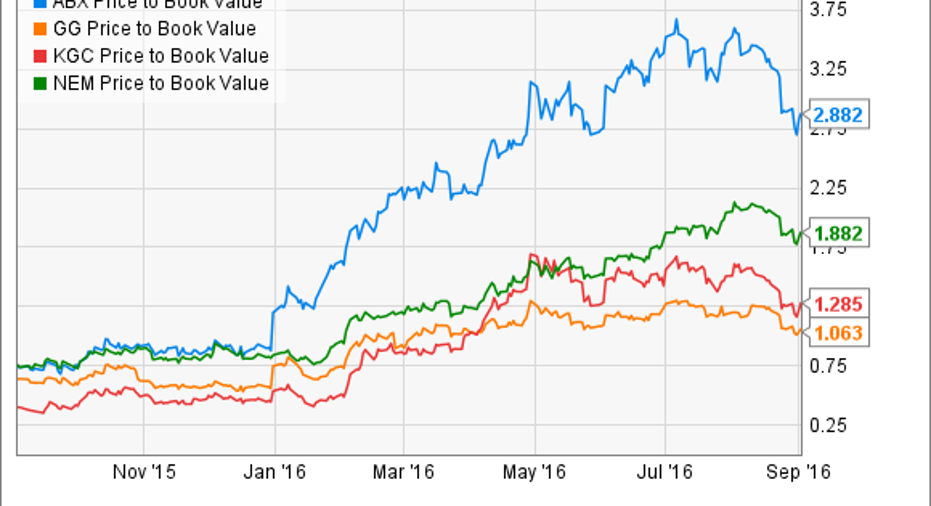

ABX Price to Book Value data by YCharts

Appearingreasonably valued in terms of sales, the stock seems equally overvalued in terms of the company's book value. Interestingly enough, the market is paying a hefty price for the company's assets, the value of which are on a steep decline from writedowns as we saw earlier.But we must remember the hefty write downs which management has been taking for the past four years. Clearly, the company's inability to effectively value its tangible assets -- like overpaying for acquisitions and accumulating goodwill -- is resulting in a skewed book value. So investors must take the stock's valuation, in terms of its book value, with a few grains of salt.

The takeaway

Valuing a company's stock is far from simple. Having taken a long look at Barrick Gold, one should hardly be compelled to pick up shares. On the other hand, there's no reason to quickly dismiss this stock. Instead, one would be best suited to put this stock on hold or a watchlist. There are likely better gold-mining stocks out there, you'll just have to mine the market to find them.

A secret billion-dollar stock opportunity The world's biggest tech company forgot to show you something, but a few Wall Street analysts and the Fool didn't miss a beat: There's a small company that's powering their brand-new gadgets and the coming revolution in technology. And we think its stock price has nearly unlimited room to run for early in-the-know investors! To be one of them, just click here.

Scott Levine has no position in any stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.