The 3 Best Pharmaceutical Stocks to Buy in 2017

One big benefit that comes from owning pharmaceutical stocks is that their products remain in demand even during periods of economic stress. That allows drugmakers to crank out profits even when the economy catches a cold.

So what pharmaceutical stocks should investors buy this year? Here's why I think thatPfizer (NYSE: PFE), Teligent (NASDAQ: TLGT), and Neurocrine Biosciences (NASDAQ: NBIX) are excellent choices.

Image source: Getty Images.

Bigger is better

Conservative investors should gravitate toward pharma companies that offer a diversified revenue stream, modest growth potential, and shareholder-friendly management teams. Those criteria perfectly match Pfizer's traits.

Pfizer racked up more than $52 billion in totalsales last year by offering dozens of differentiated products all around the world. The company's lineup includes a number of legacy products that will likely see declining sales in the years ahead due to generic competition -- think Lipitor, Norvasc, Lyrica -- as well as a few recent launches that promise rapid growth, such as Xeljanz, Eliquis,Ibrance, and more. When combined with the additional sales that will be brought in from the recent acquisitions of Hospira, Anacor Pharmaceuticals, and Medivation, Pfizer has all the ingredients it needs to post consistent single-digit revenue growth from here.

With an ever-expanding top line, Pfizer's management team should easily be able to continue its tradition of sharing the wealth with investors. That means that shareholders can expect the company's dividend payment to continue to grow and the share count to periodically shrink. That's a formula that should drive meaningful shareholder value in the years ahead.

A winning strategy

Each year several top-selling pharmaceutical products lose patent protection. That opens up the door for generic-drug makers to swoop in and steal market share.

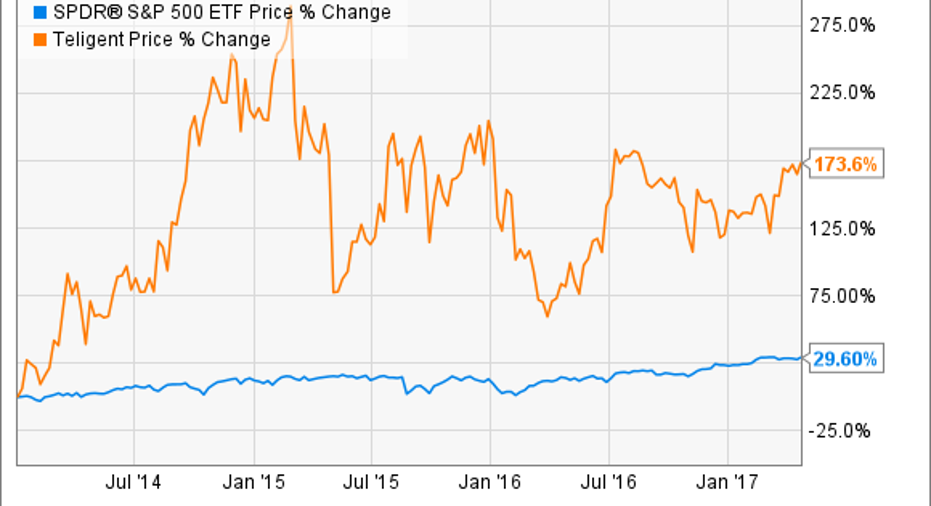

One generic-drug maker that I think is worth owning is Teligent. I like that this company doesn't focus on small-molecule drugsbut instead makes generic drugs from topical, injectable, complex, and ophthalmic markets -- think creams, lotions, and ointments. Teligent's strategy is to scan for brand-name drugs from these markets that have lost their patent protection, make a copycat, and then submit it for regulatory approval. Once it gets the green light for a formulation, it sells it on pharmacy shelves at a discount.

This simple but effective plan has worked out beautifully for investors. Sales nearly doubled between 2014 and 2016 as new products came to market, taking investors on a highly lucrative ride.

In the quarters ahead, investors should expect the good times to continue. Teligent submitted 12 new applications to the Food and Drug Administration (FDA) for review in 2016, bringing its total backlog up to 35 product candidates. Management estimates that those products have a total addressable market of$2 billion, which is quite a large opportunity for a company that only produced $66 million in revenue last year.

While this stock isn't for the faint of heart, if you're looking for a pharmaceutical company that offers upside potential, Teligent could be it.

One step ahead of the competition

Investors in the mid-cap biopharma Neurocrine Biosciences recently received the exciting news that its drug, Ingrezza, has officially been cleared for sale as a treatment for tardive dyskinesia. Tardive dyskinesiais a side effect ofantipsychotic medications that causes involuntary movements of the face and/or body that can't be controlled.

Ingrezza is the first FDA-approved drug to treat thisrare disorder, which means the company should benefit from strong demand right out of the gate. Market watchers even think that this drug could eventually top $1 billion in peak sales.

The only potential wrinkle here is that Israeli pharma giantTevaPharmaceutical Industries(NYSE: TEVA)has a tardive dyskinesia drug, calledAustedo, that is currently under FDA review. Austedo already got the thumbs-up from the agency as a treatment for chorea associated with Huntington's disease, and it has received priority reviewfor treating tardive dyskinesia. Those factors mean that the odds of nabbing an approval on its decision date in late August of this year look to be quite good. However, Ingrezza would likely still hold an edge over Austedo since the latter carries a black-box warning for depression and suicidal thoughts. That contraindication isn't on Ingrezza'slabel, which should give it a clinical edge.

Neurocrine Biosciences also boasts an exciting late-stage pipeline that holds a lot of potential. The company is currently in phase 3 trials with drugs that treat could potentially treat diseases like Parkinson's, endometriosis, and uterine fibroids. The company is also studying Ingrezza as a possible treatment of Tourette syndrome. While success in these other indications is far from guaranteed, I like that investors have a few more shots on goal.

Between Ingrezza and its late-stage pipeline, Neurocrineoffers investors a lot of upside potential. That makes this high-risk biopharma stock worth owning, in my view.

10 stocks we like better than PfizerWhen investing geniuses David and Tom Gardner have a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

David and Tom just revealed what they believe are the 10 best stocks for investors to buy right now... and Pfizer wasn't one of them! That's right -- they think these 10 stocks are even better buys.

Click here to learn about these picks!

*Stock Advisor returns as of April 3, 2017

Brian Feroldi has no position in any stocks mentioned. The Motley Fool recommends Teva Pharmaceutical Industries. The Motley Fool has a disclosure policy.