The 3 Best Ways to Profit From Low Interest Rates

Here are some ways to turn low percents into dollars and cents. Image source: Getty Images.

Interest rates are about as cheap today as they've ever been:

Overnight Federal Funds Rate data by YCharts

This is great in a lot of ways, making loans and financing cheaper for almost everything. But at the same time, lower rates aren't good for savers and investors, reducing the yields on savings, certificates of deposit, and fixed-income investments like bonds. What's an investor to do?

We asked three of our top contributors to chime in on this topic, and they gave us three different ways that low interest rates have created opportunities, including lowering (and locking in) your housing costs, investing in the strong demand for new homes after years of minimal building, and buying high-quality bank stocks while the market is beating up the sector.

Read on if you're ready to put low interest rates to work for you.

Take advantage of historically cheap mortgage rates

Selena Maranjian: The low interest rates we've had for many years now have made it hard for savers to earn meaningful interest in low-risk bank accounts and in CDs. Even bond income is depressed, too. A big group of people have benefited from them, though: Those who have bought homes. After all, the lower the interest rate, the more affordable the mortgage.

Check out the following table, in order to appreciate just how much of a difference the interest rate makes. It offers monthly mortgage paymentsat various interest rates for someone who buys a $250,000 house, who put $50,000 down and borrowed $200,000 on a 30-year fixed-rate mortgage. (It also excludes taxes, insurance, and other expenses.)

|

Interest Rate |

Monthly Payment |

Total Interest to Be Paid |

|---|---|---|

|

4% |

$955 |

$143,739 |

|

5% |

$1,074 |

$186,512 |

|

6% |

$1,199 |

$231,676 |

|

7% |

$1,331 |

$279,018 |

|

8% |

$1468 |

$328,310 |

With interest rates much more likely to increase than decrease in the coming years, this is a great time to buy a home if you've already been seriously considering it. A difference of just a single percentage point in your loan's interest rate can cost you more than $40,000 over the life of your loan! Higher monthly payments due to higher interest rates can also force you to settle for a smaller or less wonderful house.

If you are thinking of buying a home or are considering refinancing, read up on the topic for more tips that can save you many thousands of dollars. For example, shop around for the best rate you can get, but also look for borrower-friendly terms, such as no penalties for making extra payments. Get your credit score as high as possible, too, as that can also get you a lower rate.

If you're not in the market for a home, that's OK. Buying a home offers many benefits, but in general, it has not proven to be a better way than the stock market to grow your wealth.

Invest in a rising real-estate market

Dan Caplinger: Just as Selena discusses, low interest rates make it easier than ever for people to spend money on high-ticket items like housing. Yet if you don't want to make a personal commitment to real estate, you can instead put your portfolio money to work in companies that will benefit from a strong real-estate market.

The most obvious beneficiaries of low interest rates are homebuilder stocks, because companies that build homes do better when sales are high. Low rates support higher prices, and they make it easier for purchasers to qualify for loans that are large enough to help them afford homes even in rising markets. Individual homebuilders have done well, and the broader-based SPDR Homebuilders ETF (NYSEMKT: XHB) offers a diversified set of homebuilder stocks for your convenience.

Yet you can also find stocks that benefit from second-order effects of a solid housing market. For example, building materials stocks like USG Corp. (NYSE: USG) have performed well during 2016, with the maker of gypsum materials seeing strong demand for products like its Sheetrock drywall and panels. Other home-construction-related companies have also reported high interest in similar products.

As long as the housing industry does well, companies like these should see continued success. Low rates will be an integral part in determining how long the new housing boom can last.

Invest in these solid banks while they're on sale

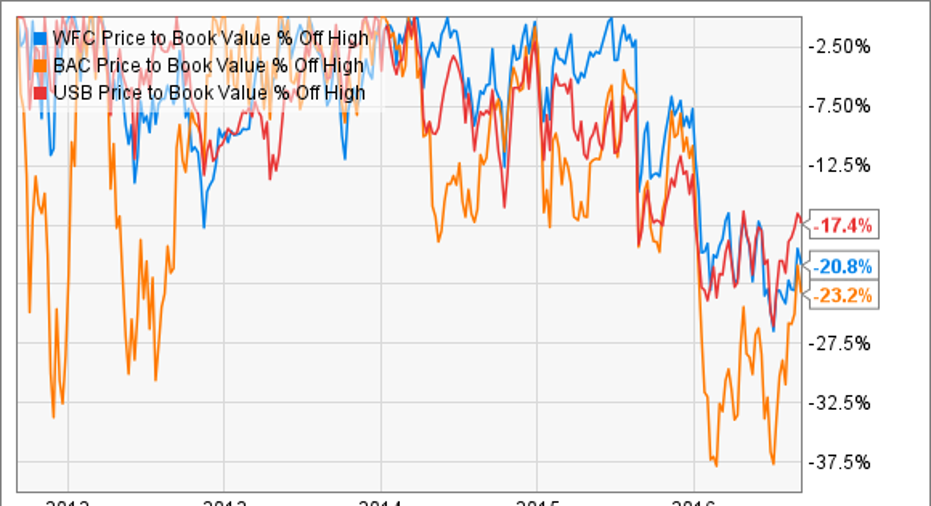

Jason Hall: It may seem counterintuitive to invest in an industry that benefits from high interest rates and loses some advantage when rates are low. But the current interest rate environment has been a big factor in creating an excellent opportunity for investors:

WFC Price to Book Value data by YCharts

U.S. Bancorp(NYSE: USB),Wells Fargo & Co(NYSE: WFC), andBank of America(NYSE: BAC)are three high-quality banks that have seen their share prices and valuations fall sharply over the past year or so largely on the global macroeconomic concerns that have played a big role in keeping interest rates so low.

The thing is, all three of these companies are solidly profitable in the current environment, and selling at or near the bottom of the interest rate cycle is a great way to miss the real opportunity: Owning these banks when interest rates start going back up.

If you're looking to profit from the current low interest rate environment, I can't think of a better way than buying these high-quality banks at a solid discount while rates are still low.

A secret billion-dollar stock opportunity The world's biggest tech company forgot to show you something, but a few Wall Street analysts and the Fool didn't miss a beat: There's a small company that's powering their brand-new gadgets and the coming revolution in technology. And we think its stock price has nearly unlimited room to run for early in-the-know investors! To be one of them, just click here.

Dan Caplinger has no position in any stocks mentioned. Jason Hall owns shares of Bank of America and Wells Fargo. Selena Maranjian has no position in any stocks mentioned. The Motley Fool owns shares of and recommends Wells Fargo. The Motley Fool has the following options: long October 2016 $50 calls on Wells Fargo. The Motley Fool recommends Bank of America. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.