This one assumption could make you run out of money in retirement

Retirement can be a lot harder if you make investment assumptions with numbers that are just a little off

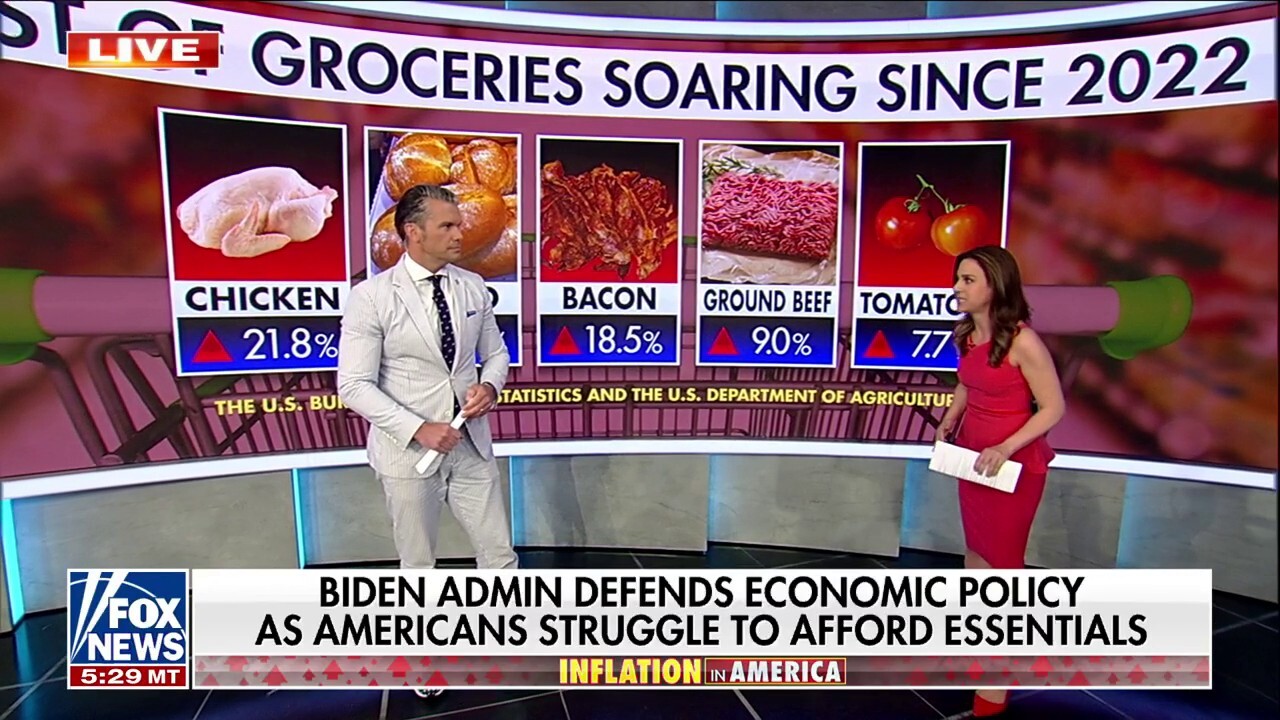

Energy policy under Biden explains 'a lot' of inflation questions: Jackie DeAngelis

'The Big Money Show' co-host Jackie DeAngelis discusses the current impact of inflation as the Biden administration defends its economic policies.

We all know that prices aren’t coming down. They are just going up slower. With the worst four years of inflation since the 1970s inflation has averaged more than 5% per year during the Biden administration. While most of us think about inflation with the cost of gas prices, the grocery store, dining out, vacation and car insurance, most Americans haven’t considered how this may impact their financial plan for the future.

Guess what? Neither has your financial advisor.

Years ago, when your financial advisor told you that you were on track to be able to retire at the age of 60 or 62 or 65 years old, what were the assumptions they used for your financial plan? The assumptions made within your financial plan can be very conservative or very aggressive depending on your viewpoint about planning for your retirement.

PRESCRIPTION DRUG PRICES HAVE SURGED ALMOST 40% OVER THE PAST DECADE

To be clear, it is something you should be revisiting regularly because making minor errors in your overall plan can lead to major catastrophes over the long-term, including you holding a bag in your 70s or 80s that has no money. Here are three key assumptions that you should be revisiting right now:

Miami Beach Florida, Collins Avenue, The Vacation Supply Company, window display sign inflation relief sale. (Photo by: Jeffrey Greenberg/Universal Images Group via Getty Images / Getty Images)

1. Inflation

Most of the financial planning software available gives you or a financial advisor a chance to assume a certain inflation rate. If the software only uses whole numbers, then you have a problem with your financial plan already. The difference between using 2% or 3% and 4% is astronomical when it comes to calculating your overall retirement numbers.

From January 1992 to January 2012, inflation grew at a total 20-year rate of 64.13% (average 3.21%). In the past five years, the average inflation rate was 4.32%. The problem with most financial plans is that they use a whole number of 3% to conclude you need less money in retirement.

The difference between using a 3.0% and 3.25% inflation rate within a financial plan can literally mean more than an extra $500,000 over a 30-year time frame necessary to reach your retirement goal. It’s what could leave you in a position to run out of money in retirement.

2. Rate of return on your money

Most of you who have put money in your 401(k)s over the last decade have likely noticed that your increases have strictly come from your extra contributions from you and your employer.

Retirees forced to return to work amid inflation

Joyce Fleming and Greg Piazza discuss being forced to return to the workforce due to rising costs.

Every financial plan will ask you to make a data entry on the expected rate of return on your assets. You can choose to tell the computer that you will earn 4%, 6%, 8%, etc. on your retirement assets. Remember that with the simple rule of 72, you can generally tell how long it will take for your original principal to double.

If you choose 10% as a rate of return assumption, it will only take 7.2 years for your original money to double. If you use 4%, it will take a whopping 18 years for your money to double in value. I see far too many financial plans done by firms showing clients should be able to earn 8% or 10% in the retirement section of their financial plans.

GET FOX BUSINESS ON THE GO BY CLICKING HERE

This is a huge mistake. By using something more conservative in the 5% or 6% range, you will give yourself a more realistic view about how much you really need to save for retirement.

3. Taxes

With the wrong tax assumptions, you could also put a major pothole in your retirement plan. Have you thought about what state you want to live in at retirement? Will it be a high tax state, a low tax state, or a no-tax state? Have you considered not only your asset allocation for investing but also your tax allocation?

The difference between using a 3.0% and 3.25% inflation rate within a financial plan can literally mean more than an extra $500,000 over a 30-year time frame necessary to reach your retirement goal. It’s what could leave you in a position to run out of money in retirement.

Federal tax rates can be used with marginal or effective rates which means the tax rate on the last dollar of earned income you bring in or your overall tax rate. You should consider using the effective tax rate based upon the income you are projecting to earn throughout retirement.

Remember, the higher the federal tax rate you use, the more dollars you will need to save for retirement. Don’t forget if the state you retire in has personal property taxes or other taxes that need to be considered in the overall analysis. Many financial plans have default tax assumptions which financial advisors don’t even bother paying attention to when they run the numbers. Another huge mistake that people make with their overall retirement plan.

CLICK HERE TO READ MORE ON FOX BUSINESS

There are many other assumptions that can go wrong or right, including health care assumptions and overall expense consideration where mistakes can be made, but these are the big three that you should be asking deeper questions about whether you do your own financial plan or hire a professional to do one for you.

Knowing how to make conservative assumptions can give you much more margin for error as you develop your retirement plan over your lifetime. Right now, the one mistake of miscalculating an inflation assumption could be the difference between you having enough money to enjoy a prosperous retirement or falling back on the danger of Social Security being the mainstay of your retirement income.