3 ways to clean up your finances this Labor Day

Labor Day 2021 is a great time to reflect on your summer spending and create a debt repayment plan. Here are three things you can do to reduce debt and improve your personal finances. (iStock)

Labor Day marks the unofficial end of summer — and summer 2021 was a time of overspending, with revolving credit card debt growing by 11.4% in May and 22.0% in June, according to the Federal Reserve. Overall, household debt surged by $313 billion in Q2 2021, rising 2.1% from the first quarter, suggesting that consumers increased their borrowing when it comes to mortgages and student loans in addition to credit cards.

Now that the high season of spending has come to an end, it's a good time for borrowers to evaluate their finances and find ways to save money. Here are three things you can do during Labor Day 2021 to set yourself up for financial success for the rest of the year:

- Pay down credit card debt

- Shop for a lower mortgage rate

- Refinance your student loans

You can compare a number of financial products on Credible's marketplace so you can get the lowest rate possible for credit card consolidation, mortgage refinancing and student loan refinancing.

DEBT AVALANCHE VS. DEBT SNOWBALL METHOD: WHAT'S THE DIFFERENCE?

Pay down credit card debt

While many Americans took advantage of downtime during the coronavirus pandemic to pay down their credit card debt, consumers fell into old spending habits during summer 2021. Revolving consumer credit increased to $992.2 billion in June 2021, increasing at a seasonally adjusted annual rate of an astounding 22%.

Credit cards typically have the highest interest rate among popular financial products, which can cause the balance to skyrocket if you're just making the minimum payments. After a summer of overspending, take some time this Labor Day to create a debt payoff plan. One popular credit card debt repayment strategy is to take out a personal loan.

HOW TO GET A DEBT CONSOLIDATION LOAN WITH BAD CREDIT

Personal loans offer fast, lump-sum funding that you can use to pay off unpredictable credit card debt. Unlike credit cards, personal loans are repaid in fixed, monthly installments — which means you'll always know how much you owe. They also tend to come with much lower interest rates than credit cards. The average personal loan interest rate is 9.58%, according to the Fed, whereas the average rate for credit accounts assessed interest was 16.30%.

Because they come with lower fixed rates, personal loans can help consumers save money while repaying their credit card debt on a consistent schedule. Borrowers who consolidated credit card debt into a personal loan using Credible's marketplace in May 2020 saw a potential savings of nearly $2,400 on average.

See how much money you can save by paying off high-interest credit card debt using Credible's personal loan calculator.

HOW TO GET A BALANCE TRANSFER CREDIT CARD

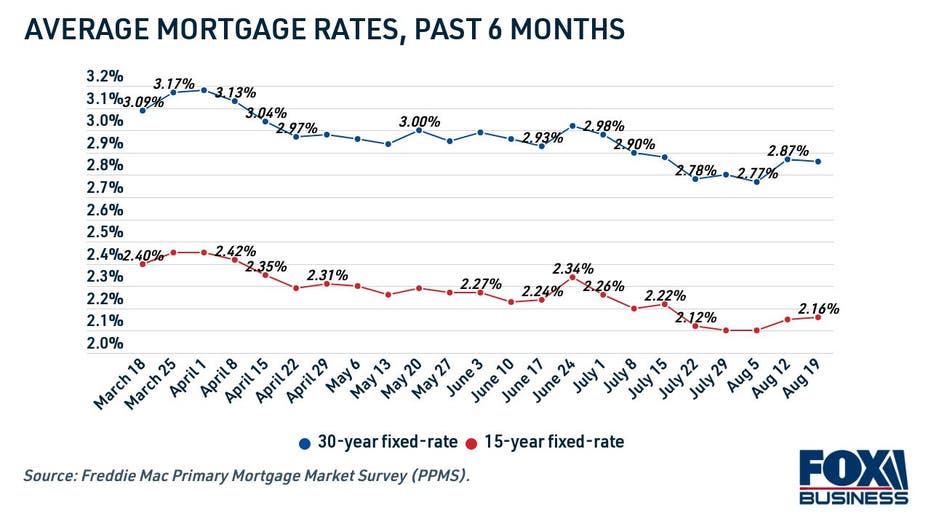

Shop for a lower mortgage rate

Mortgage rates are still near historic lows, which means refinancing should be a no-brainer if you own a home. Plus, mortgage refinancing is now cheaper than ever with the recent elimination of a 0.5% pandemic-era refinancing fee. But despite such favorable conditions, millions of homeowners still haven't yet refinanced their mortgages.

Mortgage rates are holding steady below 3%, according to data from Freddie Mac.

7 SMALL PERSONAL LOANS TO CONSIDER IF YOU NEED SOME EXTRA CASH

Mortgage refinancing can save you tens of thousands of dollars over time, in addition to helping you pay off your mortgage faster and lowering your monthly payments. You can use a mortgage payment calculator to estimate the terms of your new mortgage, including your mortgage payment and total interest paid.

It's important to shop around for the lowest mortgage refinance rate for your unique situation so you can save the most money possible over the life of your home loan. You can compare mortgage rates without impacting your credit score on Credible.

WHAT TO DO IF YOU CAN'T MAKE YOUR MINIMUM MONTHLY PAYMENT ON YOUR CREDIT CARDS

Refinance your student loans

Private student loan refinancing can help you lower your monthly payments, pay off your debt faster and save money on interest over time. And since student loan refinance rates are also hovering around record lows, now is a great time to pay off your private student loan debt at a lower interest rate.

Looking to lower your monthly payments? Well-qualified borrowers who refinanced their student loans to a longer term on Credible were able to save more than $250 on their student loan payments without having to pay more in interest over the life of the loan.

DEBT CONSOLIDATION VS. DEBT SETTLEMENT: WHAT'S THE DIFFERENCE?

If you want to pay off your student loans faster, consider refinancing to a shorter-term loan. Borrowers who refinanced to a shorter loan term on Credible saved nearly $17,000 over time and shaved 41 months off their loan repayment term.

There is a caveat, though: Refinancing your federal student loans to a private loan makes you ineligible for federal protections like income-driven repayment, COVID-19 forbearance and even student loan forgiveness programs. But if you have private student loan debt, you have nothing to lose by refinancing to a new private student loan at a lower interest rate.

See if you qualify for a lower rate on your student loans by getting prequalified through multiple private lenders on Credible's marketplace.

SENATE BILL TARGETS STUDENT LOANS IN BANKRUPTCY

Have a finance-related question, but don't know who to ask? Email The Credible Money Expert at moneyexpert@credible.com and your question might be answered by Credible in our Money Expert column.