Failure to lift debt ceiling may cause mortgage rates to rise, report finds: Why you should refinance now

If Congress fails to raise or suspend the debt ceiling and the federal government defaults on its financial obligations, it will have a tangible economic impact. Stock prices will fall and interest rates will rise, according to Moody's Analytics. Her (iStock)

The federal government may soon default on its financial obligations unless Congress works to raise or suspend the debt ceiling before the Treasury Department runs out of funding on Oct. 18, estimates Treasury Secretary Janet Yellen.

The United States has never defaulted on its debt, and the consequences to the country's credit rating would be far-reaching, according to a new report from Moody's Analytics. The economy could spiral into an economic downturn, eliminating 6 million jobs and wiping out $15 million in household wealth. Stock prices could be cut in half, and interest rates could rise across the board.

"Treasury yields, mortgage rates, and other consumer and corporate borrowing rates spike, at least until the debt limit is resolved and Treasury payments resume," the report reads. "Even then, rates never fall back to where they were previously."

Since U.S. Treasury securities no longer would be risk free, future generations of Americans would pay a steep economic price.

WHAT YOU NEED TO KNOW BEFORE MAKING A DOWN PAYMENT ON A HOUSE

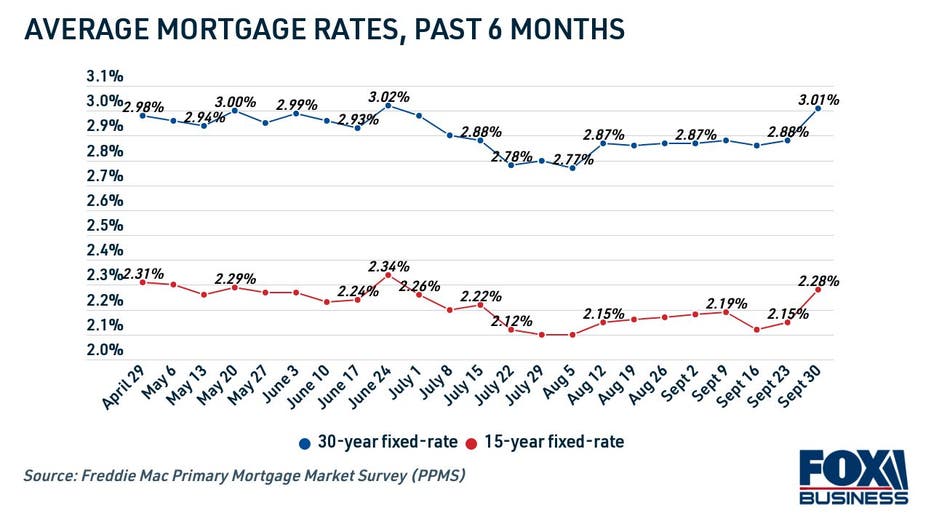

Mortgage rates are still currently near historic lows, although they've been creeping up in the past few weeks. So if you've been thinking about taking out a home loan or refinancing your current mortgage, you don't have time to wait.

Keep reading to learn why it's a good time to lock in a low mortgage rate, and visit Credible to compare rate quotes across multiple mortgage lenders without impacting your credit score.

VETERANS BORROWING VA LOANS AT A RECORD PACE, STUDY SHOWS

Today's mortgage rates won't be around forever

Mortgage rates have been hovering around 3% since July 2020, according to Freddie Mac. But this environment of dirt-cheap mortgage interest rates can't last forever, which means now is the right time to act if you're thinking about buying a home or refinancing your current mortgage.

WHAT ARE THE NEW FHA LOAN LIMITS FOR 2021?

With the Federal Reserve set to implement a rate hike in 2022, economists forecast that mortgage rates will rise soon. The Mortgage Bankers Association (MBA) predicts 30-year rates will increase to 4.0% in 2022 and 4.3% in 2023.

In contrast, today's mortgage rates are hovering slightly above 3%. You can browse interest rates from real mortgage lenders in the table below. To see what kind of mortgage rate you qualify for, get prequalified on Credible in just minutes.

EVERYTHING YOU NEED TO KNOW ABOUT REFINANCING A FEDERAL HOUSING ADMINISTRATION LOAN

How to lock in a low mortgage rate

Now is the time to take advantage of low current mortgage rates, whether you choose a 15-year adjustable-rate mortgage or 30-year fixed-rate loan. Here's how you can secure your low mortgage rate now:

- See where your credit score stands. The higher your credit score, the lower the mortgage rates you'll qualify for. Credible recommends a minimum credit score of 620 to refinance your mortgage or take out a new home loan.

- Work on building your credit score. If you have a poor credit score, defined by the FICO model as 580 or lower, you'll want to try to raise it before applying. You can sign up for free credit monitoring on Credible to keep an eye on your progress.

- Compare rates from multiple lenders. Most mortgage lenders let you prequalify for a mortgage, which allows you to check potential mortgage rates and monthly payments with a soft credit inquiry. This way, you can shop around among multiple lenders to find the best deal.

- Choose the lender with the best offer. The best mortgage offer will likely be the one with the lowest interest rate, because a lower rate translates to big savings over the long time span of a mortgage loan.

- Formally apply through the lender. Once you've decided on the best mortgage lender for your needs, you'll formally apply. The mortgage loan officer will conduct a hard credit inquiry to determine your actual rate and will want you to provide financial and identification information.

WHAT IS PRIVATE MORTGAGE INSURANCE (PMI) AND HOW DOES IT WORK?

Whether you're considering a new mortgage purchase or refinancing your current home loan, you'll need to pay loan origination fees like closing costs, which are typically about 1.5% of the total loan amount. Closing costs can usually be rolled into the mortgage loan, and they impact the annual percentage rate (APR) or the total yearly cost of the loan.

You can get prequalified through multiple mortgage lenders in one place on Credible's online marketplace. Once you have a good idea of your estimated interest rate, use a mortgage calculator to estimate your new mortgage payments.

HAVE BAD CREDIT? YOU MIGHT BE OVERPAYING FOR HOMEOWNERS INSURANCE, STUDY FINDS

Have a finance-related question, but don't know who to ask? Email The Credible Money Expert at moneyexpert@credible.com and your question might be answered by Credible in our Money Expert column.