3 in 4 homebuyers and sellers say inflation has impacted their plans, Redfin survey finds

Here's how to combat inflation if you're considering buying or selling a home in 2022

Inflation is influencing residential real estate decisions, causing some homebuyers and sellers to delay plans in the next year amid high prices and low housing stock. (iStock)

Inflation is at its highest level in nearly four decades, and rising consumer prices are causing homebuyers and sellers to delay, speed up or cancel their plans.

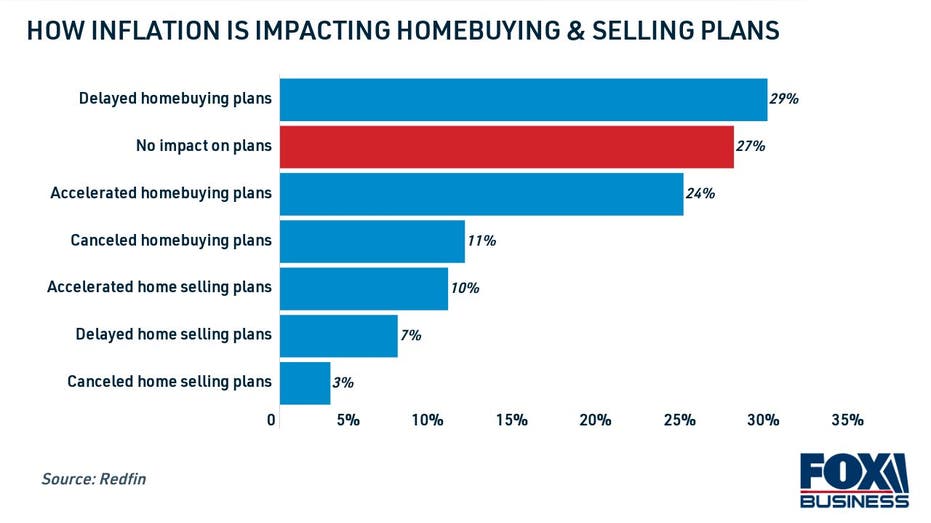

About three-quarters (73%) of homebuyers and sellers have changed their future plans due to inflation, according to a survey from real estate company Redfin. Notably, 29% of buyers have delayed their homebuying plans amid rising prices, while 24% plan on buying a home sooner in hopes of locking in a good price before inflation worsens.

HOME SALES HAVE LARGEST DROP IN OVER A DECADE

Inflation can impact Americans' financial decisions in a variety of ways, including homebuying, according to Redfin chief economist Daryl Fairweather.

"Some people may delay buying because they’re worried that with prices rising on everything from food to fuel, now is not the right time to make a huge purchase," Fairweather said. "But others might move faster to find a house because they’re worried home prices and rent prices will increase even more, and they want to lock in a fixed payment."

Keep reading to learn more about how inflation affects the housing market, as well as what prospective homebuyers and current homeowners can do to combat rising prices. If you're considering buying a home or refinancing your mortgage amid record-high inflation, visit Credible to compare mortgage rates for free without impacting your credit score.

AMERICA'S HOTTEST HOUSING MARKETS ARE IN THE SUBURBS, REPORT FINDS

How does inflation affect the housing market?

Many of the same factors that are causing the fast pace of inflation are also impacting the housing market. For example, recent supply chain issues and pandemic-related labor shortages have caused consumer prices to rise, even in the construction industry.

The cost of lumber and other building materials have kept housing supply low. Home prices continue to rise as builders struggle to keep up with demand for single-family homes.

Home price growth has outpaced inflation in the past year. Between Oct. 2020 and Oct. 2021, median home prices have skyrocketed 19.1%, according to the Case-Shiller U.S. National Home Price Index. During the same time period, inflation rose 6.2% per the Consumer Price Index (CPI).

Housing prices have also increased significantly for renters. Median rental prices in the United States rose from $1,659 in Oct. 2020 to $1,858 in Oct. 2021, according to the Zillow Observed Rental Index (ZORI), which is an increase of 12% in just one year.

LOW SUPPLY OF HOMES DRIVES SELLER'S MARKET IN NOVEMBER, REDFIN FINDS

Renters can combat inflation by buying a home

When it comes to rising housing costs, homeowners have a noteworthy benefit over renters. When you buy a home and take out a mortgage, you're guaranteeing static housing payments for an extended period of time. Over time, though, rent may continue to rise several times throughout the years.

"Three or five years from now, rents would have cumulatively risen year after year, whereas someone is locking in a fixed mortgage payment during that time," said Lawrence Yun, chief economist at the National Association of Realtors (NAR).

Nearly a quarter of homebuyers have sped up their purchasing plans, the survey found, which may suggest that some renters are becoming first-time homebuyers in order to keep their housing costs predictable over a longer period of time.

If you want to buy a home to lock in a consistent housing payment, visit Credible to compare mortgage rates across multiple lenders. Then, use a mortgage calculator to estimate your monthly mortgage payments.

POTENTIAL HOMEBUYERS: 'NOW IS A GREAT TIME TO BUY' DESPITE HOUSING BUBBLE FEARS

Homeowners may consider refinancing instead of selling

About 1 in 10 home sellers have delayed or canceled their plans due to inflation, Redfin's survey found. If you're among them, then you might be considering refinancing your home loan instead of selling.

Refinancing your mortgage to a lower interest rate may help you lower your monthly mortgage payment and save money on your home loan, which can help you combat rising prices amid inflation. American homeowners have reduced their mortgage payments by more than $1.3 billion per month since the pandemic began, according to the Black Knight Mortgage Monitor Report.

Keep in mind that if you're still planning on selling your home in the next few years, then it might not be worthwhile to refinance your mortgage due to closing costs. But if you've canceled the plan to sell your home, then it's still a good time to refinance your mortgage to a lower rate.

Freddie Mac data shows that 15-year mortgage rates set a record low of 2.10% in July 2021. This shorter mortgage term is a popular choice among homeowners who are looking to refinance. While mortgage refinance rates have risen slightly since then, the time to lock in a record-low rate is running out.

Average 30-year mortgage rates are expected to be higher in 2022, according to the Mortgage Bankers Association's latest Mortgage Market Forecast. That's because the Federal Reserve is projecting a series of benchmark rate hikes in the coming year to address high inflation, each of which will cause mortgage rates to rise.

If you're considering refinancing your mortgage to combat inflation, act now to lock in a low interest rate before the Fed implements changes to its economic policies. Visit Credible to see your estimated mortgage refinance offers across multiple lenders so that you can shop around for the lowest possible rate for your circumstances.

HOW TO WIN A BIDDING WAR WHEN BUYING A HOUSE

Have a finance-related question, but don't know who to ask? Email The Credible Money Expert at moneyexpert@credible.com and your question might be answered by Credible in our Money Expert column.