Today's Jumbo Mortgage Rates

A jumbo mortgage is a home loan that exceeds the federal conforming limit — $647,200 in 2022

If you’re buying a home that costs more than the federal conforming limit, you may need a jumbo loan. Here’s what to know about jumbo mortgage rates. (Shutterstock)

Between rising house prices and the real estate market boom, the popularity of jumbo mortgages has exploded in the past few years. In fact, jumbo loan originations reached a 14-year high in 2021 by dollar volume, according to data analytics company CoreLogic.

Before you apply for one of these high-value loans, learn how jumbo loans work and how jumbo mortgage rates compare to rates for conventional home loans.

As with any mortgage, it’s a good idea to comparison shop for jumbo loan rates. Credible makes it easy to compare mortgage rates from multiple lenders.

- Today’s jumbo mortgage rates

- Historical jumbo mortgage rates

- What’s a jumbo mortgage?

- Jumbo loan requirements

- How Credible mortgage rates are calculated

- Should you get a jumbo loan?

- How to get a good jumbo mortgage rate

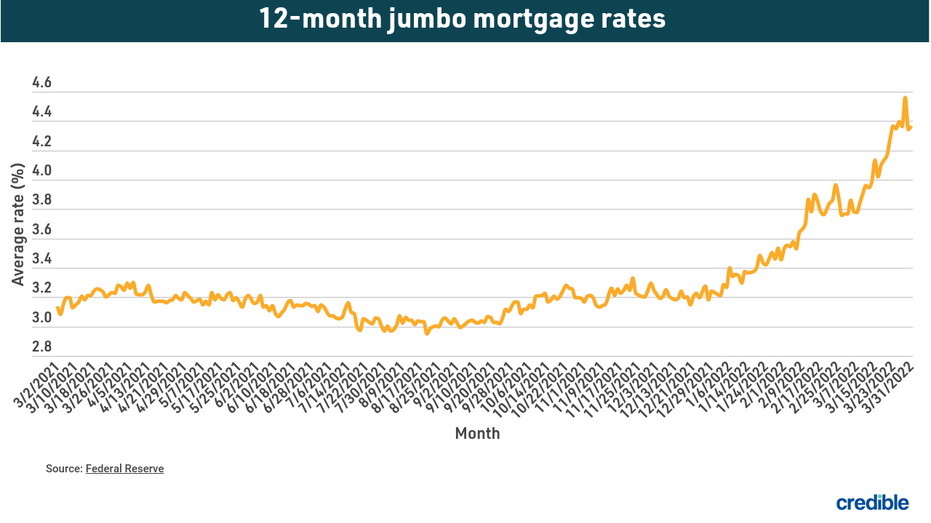

Today’s jumbo mortgage rates

Here’s a look at how jumbo mortgage rates have been trending over the past 12 months.

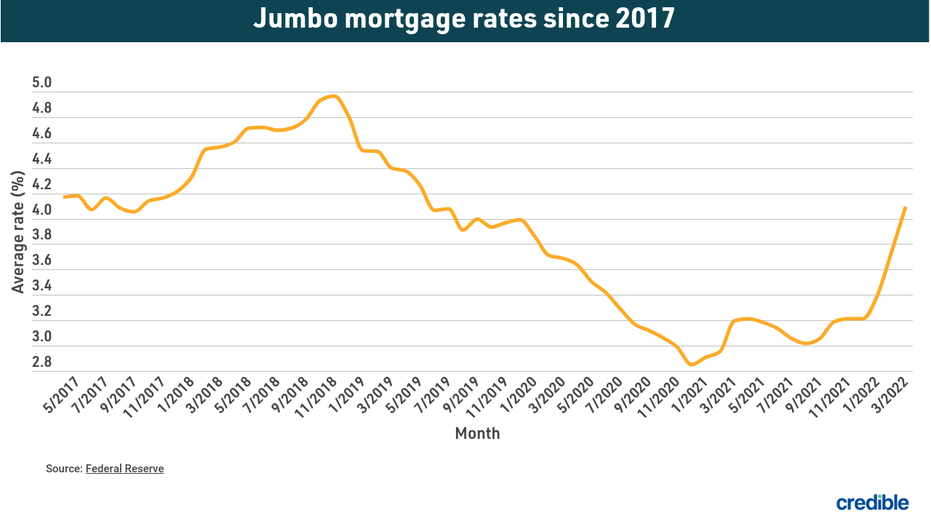

Historical jumbo mortgage rates

Here’s what jumbo mortgage rates have looked like over the past five years.

What’s a jumbo mortgage?

A jumbo mortgage is a higher-value mortgage loan that exceeds the federal conforming limit in a given year.

Each year, the Federal Housing Finance Agency (FHFA) sets a maximum mortgage loan value, known as the conforming limit. This value serves to restrict the loans that Freddie Mac and Fannie Mae are legally allowed to purchase from mortgage lenders.

A mortgage loan with an originating value above the conforming limit is considered a jumbo loan, or non-conforming loan. To determine this number, the FHFA uses a formula established by the Housing and Economic Recovery Act, which takes into account average home sale prices in the U.S.

Conforming loan limits vary by county as well as the number of units in the property. For one-unit properties, the 2022 conforming limit starts at $647,200, but it can be as high as $970,800 in certain high-cost areas. Buyers who are trying to purchase a home that’s priced above the limits in their county will need to look into a jumbo mortgage loan.

Jumbo mortgage vs. conforming mortgage

As you may have guessed, a conforming mortgage loan is one that adheres (or conforms) to the conforming loan limits that the FHFA set for the county where the home is located. Fannie Mae and Freddie Mac can purchase conforming loans, so they may have less stringent qualification requirements compared to jumbo (non-conforming) loans. Conforming mortgage borrowers may have lower down payment, income, or credit score requirements, though this depends on the lender.

Conforming home loans are limited to the originating loan amounts mentioned above ($647,200 to $970,800, depending on the county). But jumbo mortgage loans don’t have an established federal loan limit to follow, meaning that eligible borrowers could use these loans to purchase property worth well into the millions of dollars.

Over the past decade or so, interest rates for jumbo loans have been at par or even lower than rates for conventional mortgages.

With Credible, you can compare conventional mortgage rates from various lenders without affecting your credit.

Jumbo loan requirements

Lender qualifications for a jumbo mortgage loan differ from those of a conventional mortgage. Since a jumbo loan represents more risk for lenders, they’ll typically require borrowers to meet more stringent requirements than if they were applying for a conforming 15-year or 30-year mortgage.

- You’ll usually need to have very good credit. Actual score requirements vary by lender, but jumbo lenders will typically expect you to have a high credit score — often well into the 700s.

- You should be prepared to show strong cash reserves. Since the lender is assuming more risk with a jumbo loan, it’ll typically expect you to have ample savings. In many cases, you may need to have enough savings to cover six to 12 months’ worth of mortgage expenses.

- You’ll need to have a qualifying DTI. Jumbo lenders often set maximum debt-to-income ratio requirements that are lower than those for conforming loans. Your DTI ratio is how much of your gross monthly income goes toward your debt payments. If your DTI ratio is too high, it may signal to lenders that you could have trouble taking on such a large mortgage.

- You may need a larger down payment. Conforming loan lenders may have down payment requirements as low as 0% or 3.5%. But jumbo loan lenders often require a much higher down payment to qualify for a loan.

How Credible mortgage rates are calculated

Changing economic conditions, central bank policy decisions, investor sentiment, and other factors influence the movement of mortgage rates. Credible average mortgage rates and mortgage refinance rates are calculated based on information provided by partner lenders who pay compensation to Credible.

The rates assume a borrower has a 740 credit score and is borrowing a conventional loan for a single-family home that will be their primary residence. The rates also assume no (or very low) discount points and a down payment of 20%.

Credible mortgage rates will only give you an idea of current average rates. The rate you receive can vary based on a number of factors.

Should you get a jumbo loan?

Whether or not you should get a jumbo loan depends on the home you want to buy and if you can meet a lender’s eligibility criteria. If you want to buy a home that costs more than the conforming loan limit in your area, you’ll likely need to take out a jumbo loan.

If you want to avoid a jumbo loan, consider these options:

- Make a larger down payment. If your loan amount is relatively close to the conforming limit in your area, you may be able to avoid taking out a jumbo loan simply by making a larger down payment. This could potentially reduce your originating loan amount enough that you qualify for a conforming loan.

- Apply for a piggyback loan. Commonly known as an 80-10-10 loan, a piggyback loan can cover a portion of your down payment, allowing you to further reduce your originating loan amount. With this second mortgage loan, you can potentially dip back below the conforming loan limit in your area — avoiding a jumbo loan altogether. You may also be able to avoid the private mortgage insurance (PMI) that’s required with a down payment of less than 20%.

- Take out a no-limit VA loan, if you’re eligible. As of 2020, loans through the Department of Veterans Affairs have no maximum limit, as long as the borrower qualifies through the specific lender. While this is a possible alternative to a jumbo loan, VA loans are limited to eligible active-duty and veteran service members.

How to get a good jumbo mortgage rate

Lenders look at certain factors when reviewing a mortgage application. These factors determine your loan eligibility, and they can also influence what interest rate lenders will offer you for a new loan.

To increase your chances of getting the best jumbo mortgage rates, you should ideally have the following:

- A large down payment

- A good credit score

- A low debt-to-income ratio

- Strong cash reserves

- Qualifying income

The specific requirements will vary from one lender to the next, and a strength in certain factors can help when you have a weakness in other factors. For example, a larger down payment can sometimes help your case if you have a lower credit score.

If you’re considering a conventional mortgage, Credible lets you easily compare mortgage rates in minutes.

Refinancing a jumbo mortgage

The decision to refinance any mortgage is a very personal one, and jumbo mortgage loans are no exception. If you currently have a jumbo mortgage and would like to lower your monthly mortgage payments, here are a few situations when you might consider refinancing:

- You have enough equity in the home now. If you’ve built up enough equity in your home that a refinance loan would actually fall below the conforming loan limit, it might be worth refinancing. You could potentially take advantage of better rates with a conventional home loan.

- Interest rates have gone down. If current rates have gone down — or you’ve improved your credit score or lowered your DTI and would now qualify for better rates — refinancing can be one way to save money on mortgage interest by reducing your interest rate or lowering your monthly payments.

- Conforming limits have gone up. Each year, the conforming loan limit is adjusted to account for shifts in average home sales. This is typically an upward trend, so if your refi loan would fall below the adjusted conforming limit in your area, refinancing could make sense.