More high schoolers are saving money for clothes than college, survey finds, raising need for student loans

Here's what you should know about paying for a university education.

Although many high schoolers are saving for clothes than college, it's never too early to start thinking of college financing and a debt repayment plan. (iStock)

Preparing for college is an exciting time in a high school student's life, but many teen consumers have prioritized saving money for buying clothes over saving for college, according to a Capital One survey of more than 1,000 12-18 year-olds.

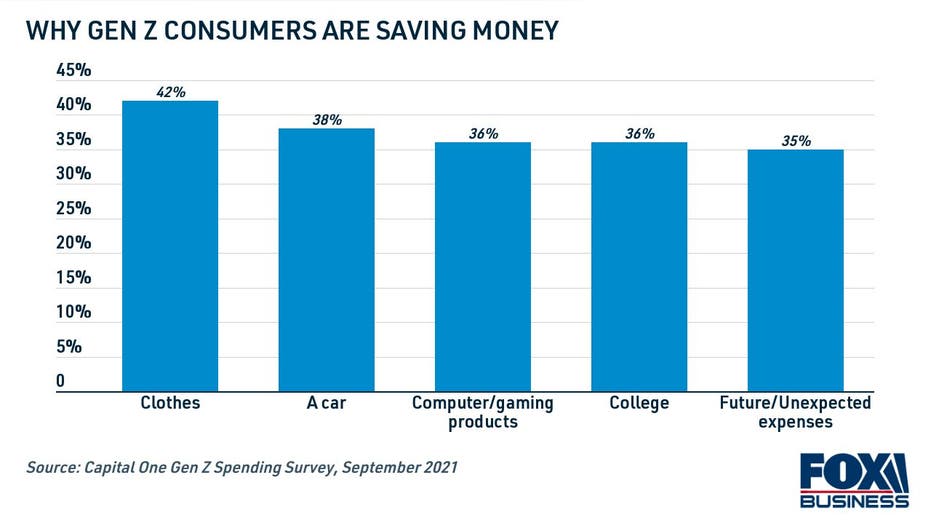

While about a third (36%) of respondents said they're saving up for college, 42% said they're saving money to buy clothes. Gen Z consumers are also saving for a car (38%), a computer or gaming system (36%) and future expenses (35%).

BIDEN ADMINISTRATION CANCELS ANOTHER $5.8B IN STUDENT LOAN DEBT: HERE'S WHO QUALIFIES

Of those surveyed, nearly 80% said they wish they were taught more about financial literacy in school.

Building a robust savings plan is an important part of paying for college. However, skyrocketing tuition costs make it difficult for students to finance higher education costs without taking on debt like student loans.

Keep reading to learn more about how rising college students can financially prepare for the years ahead, including borrowing student loans. You can learn more about private student loans and compare offers from multiple student loan lenders at once on Credible.

How to prepare your finances for going to college

Budgeting and saving for college in advance can be a good way to cut down on borrowing costs and pay less interest charges while you earn your degree. In reality, though, the cost of college is too high for most aspiring students to afford without borrowing money.

Here are a few ways you can do to prepare for the financial obligation of higher education.

EDUCATION DEPARTMENT ISSUES 'FINAL EXTENSION' OF STUDENT LOAN DEFERMENT: IS DEBT CANCELLATION NEXT?

1. Research the cost of colleges and their programs

The cost of college varies widely on the type of school you attend and the course of study you choose. Depending on the state in which you live, it might be much cheaper to attend a state-funded university than a private college.

You should also consider the cost of the degree in your field of study. A recent study by the Texas Policy Center found that some degrees are more likely to pay off in the form of higher earnings than others. For example, a computer science degree leaves graduates with $23,000 worth of student loan debt and has an average salary of $69,338. On the other hand, a degree in theater arts costs $25,000 but leads to much lower earnings at $22,781.

Get in touch with the financial aid office at the schools you plan on applying to, so that you can have a good idea of how much a degree will cost you between tuition, room and board and other expenses.

PRESIDENT BIDEN LAUNCHES INQUIRY TO FIX PUBLIC SERVICE LOAN FORGIVENESS PROGRAM

2. Apply for federal student aid

Each year, the Department of Education grants more than $120 billion worth of federal student loans, grants and work-study programs. To apply for financial aid, you have to fill out the Free Application for Federal Student Aid (FAFSA).

You can fill out the FAFSA by creating an account on the Federal Student Aid (FSA) website. The FSA also offers a complete guide for filling out the FAFSA, noting that most students can fill out the application in less than 30 minutes.

Often, federal student loans won't cover the entire cost of going to college. The Department of Education sets federal student loan limits for undergraduates based on dependency status: $31,000 for dependent students and $57,500 for independent students — and that's for your entire undergraduate tenure.

WHAT ARE THE FEDERAL STUDENT LOAN LIMITS FOR THE 2021-22 SCHOOL YEAR?

3. Consider your borrowing options if federal loans come up short

When federal student loans don't cover the entire cost of college, PLUS loans and private student loans can be a way to bridge the financing gap.

PLUS loans are federal student loans that come at a higher interest rate (6.228%), and they can only be borrowed by parents and graduate students. PLUS loans aren't an option for undergraduate students who need to borrow money to pay for college expenses, but can't rely on their parents to take out a loan on their behalf.

Private student loans are issued by a private lender rather than the federal government. Interest rates are set based on the amount of the loan and the repayment term, as well as the borrower's creditworthiness. Because private student loan rates can vary from one lender to another, it's important to shop around with multiple lenders to get the lowest possible rate for your situation.

You can browse student loan rates from real private lenders in the table below, and visit Credible to see rates tailored to you without impacting your credit score.

REFINANCING CAN LOWER YOUR STUDENT LOAN PAYMENTS BY $250: HERE'S HOW

How to save money on your student loan debt

More than 45 million Americans currently owe $1.7 trillion worth of student loan debt already, which means that many borrowers may be looking for ways to reduce the amount of debt they owe.

If you're a college graduate looking for a way to save money on your student loan debt, consider private student loan refinancing. By locking in a lower interest rate on your student loan debt, you may be able to lower your monthly payments, save money on interest and even pay off debt faster.

Creditworthy borrowers who refinanced to a shorter-term student loan using Credible were able to save nearly $17,000 and pay off their loans 41 months faster, thanks to historically low interest rates. Use a student loan refinance calculator to see how much you can save on your college debt.

Whether or not you should refinance depends on the type of loans you have. Even though you may be able to get a lower interest rate, refinancing your federal loans into a private loan makes you ineligible for federal relief measures like income-driven repayment (IDR), administrative forbearance and student loan forgiveness programs

But if you have private student loan debt, you don't risk losing these types of benefits by refinancing. Still not sure if refinancing is right for you? Get in touch with a knowledgeable loan officer at Credible to learn more about student loan refinancing.

MOST PARENTS THINK THEIR KIDS' COLLEGE COSTS WILL TOP $100K, NEW STUDY FINDS

Have a finance-related question, but don't know who to ask? Email The Credible Money Expert at moneyexpert@credible.com and your question might be answered by Credible in our Money Expert column.