Former Obama housing chief slams Biden’s ‘unprecedented’ mortgage plan: ‘Not the way to do it’

The rule would give homebuyers with riskier credit scores better mortgage rates and lower fees than homeowners with good credit

Former Obama housing chief slams ‘unprecedented’ Biden mortgage plan

Former Obama Federal Housing Association Commissioner David Stevens warns against the White House redistributing high-risk loan costs to homeowners with good credit.

Many critics have blasted new rules from the Biden administration that will force good-credit homebuyers to subsidize the costs of buyers with poor credit. One former Obama housing official is calling out the "unprecedented" move, arguing this is "not the way" to bring in more home buyers.

"This is an unprecedented move," Former Federal Housing Administration Commissioner David Stevens said on "America Reports" Thursday. "We can do better programs to help more minorities get into homeownership. This is not the way to do it."

New rules from the Federal Housing Finance Agency (FHFA) will allow consumers with lower credit ratings and less money for a down payment to qualify for better mortgage rates than they otherwise would have. In turn, the costs are expected to be passed on the those with good credit. The rules are set to go into effect May 1.

Government-sponsored enterprises (GSE) like Freddie Mac and Fannie Mae, have traditionally risk-based priced their loans. The new rules, however, will change the way those mortgages are set.

REAL ESTATE EXPERT SHREDS BIDEN RULE PUNISHING HOMEBUYERS WITH GOOD CREDIT: ‘IT’S MADNESS'

Stuart Varney: Biden’s new mortgage rule punishing homeowners with good credit is 'pure politics'

FOX Business host Stuart Varney argues homeowners with good credit will pay for their 'success.'

"For the first time ever, the [FHFA] director, in an effort to bring more first-time homebuyers - particularly minority homebuyers into the GSE's lending programs - made a shift where she lowered the fees being charged to borrowers with low down payments and low credit scores and the way she compensated or they compensated for that loss of income, that capital costs that they're going to incur, is they're actually raising fees on better creditworthy borrowers who are putting down much larger down payments," Stevens said.

US REAL ESTATE MARKET IN ‘BIG TROUBLE,' EXPERT WARNS

Experts believe that borrowers with a credit score of about 680 would pay around $40 more per month on a $400,000 mortgage under the FHFA rules – costs that will help subsidize people with lower credit ratings also looking for a mortgage, according to a Washington Times report Tuesday.

"This has really convoluted the entire discipline and credit risk pricing structure that Fannie Mae and Freddie Mac have followed since their inception," Stevens added.

"I think it violates the entire discipline that these two companies have operated under. And it's going to end up costing some borrowers who are putting in 15, 20% down payments, who have credit scores in the seven hundreds and above more for their mortgage so they can help pay for those who are getting the discount," he warned.

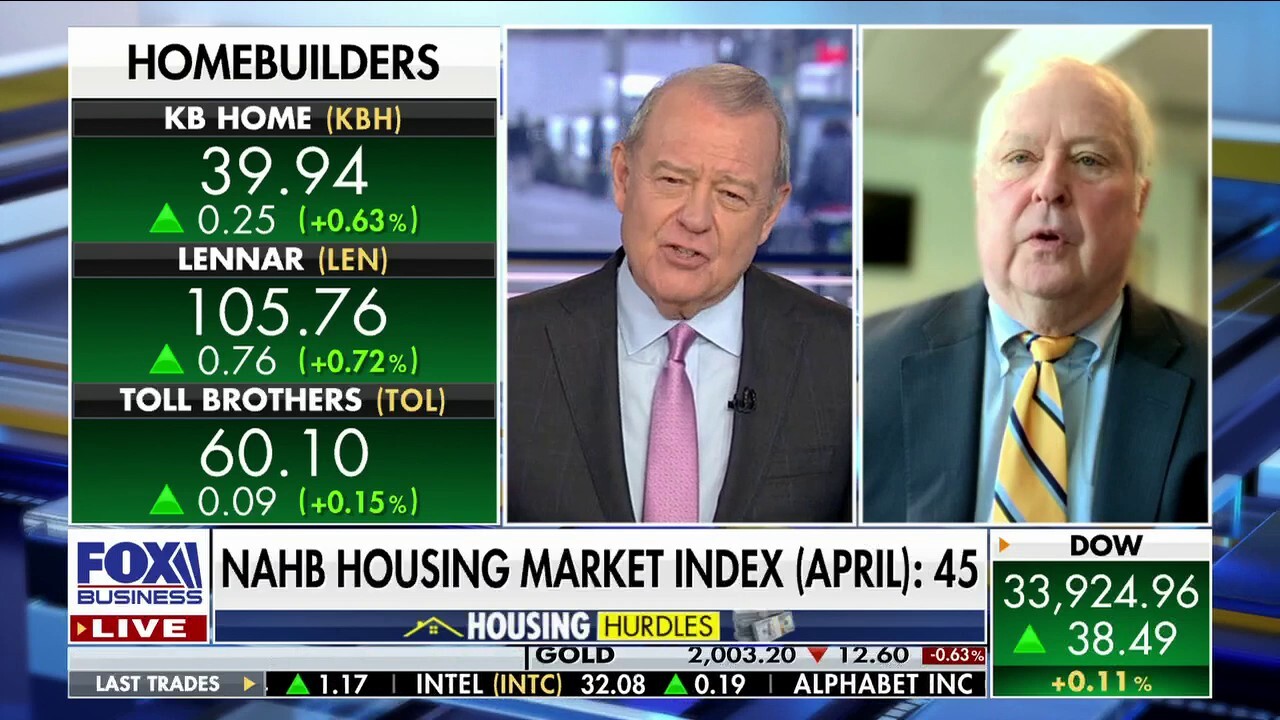

US housing market 'not operating on all cylinders' yet: Jerry Howard

National Association of Home Builders CEO Jerry Howard breaks down April's housing market index, which showed new home starts rose slightly.

The Federal Housing Finance Agency, which oversees federally backed home mortgage companies Fannie Mae and Freddie Mac, has long sought to give consumers more affordable housing options.

Federal Housing Finance Agency Director Sandra Thompson said the new rules are designed to "increase pricing support for purchase borrowers limited by income or by wealth" and come with "minimal" fee changes.

BIDEN RULE WILL REDISTRIBUTE HIGH-RISK LOAN COSTS TO HOMEOWNERS WITH GOOD CREDIT

Stevens, however, said the industry was "outraged" by the decision to use GSEs for "political purposes."

"I literally just got an email from an executive with a mortgage lending company. He goes, ‘So I guess we have to teach borrowers to worsen their credit before they apply for a mortgage in order to get the better price.’ I mean, that's a bit of an extreme, but yes, I totally recognize and appreciate the effort to bring more people into homeownership who have traditionally not had that opportunity. But using Fannie Mae and Freddie Mac for these sorts of political purposes may not be the best thing to do," Stevens said.

Like many experts, Stevens fears the rule change is "very concerning" given the state of the U.S. housing market.

Sales of previously owned homes tumbled 2.4% in March from the prior month to an annual rate of 4.4 million units, according to new data released Thursday by the National Association of Realtors (NAR). On an annual basis, existing home sales are down 22% when compared with March 2022.

A new Biden administration rule will subsidize costs for high-risk homebuyers through buyers with good credit. (AP Photo/Gene J. Puskar / AP Newsroom)

The market is also dealing with limited inventory and fewer home builds.

A recent report from Realtor.com showed that the number of available homes on the market last month is down more than 50% from the typical amount before the pandemic began.

"We're in a period where interest rates have risen. We're all seeing the home sales data and seeing how much home sales are declining because of these rising interest rates," Stevens said.

"Now we're adding this second whammy to good credit-worthy home buyers who are now going to have to pay for other people's mortgages. And that's something that I think is a real bad reaction."

CLICK HERE TO READ MORE ON FOX BUSINESS

Fox News' Michael Lee and FOX Business' Megan Henney contributed to this report.