Money Mistakes to Avoid by the Time You Reach 40

We all make mistakes but wouldn’t it be great if you could avoid some common mistakes when it comes to money. Whether fresh out of school or nearing middle age, here’s a look at some common financial errors people make by the time they hit 40 and the best ways to avoid them.

Not Saving Enough

The last thing a young person wants to think about is saving for retirement but financial advisers say it should be near the top of the list. “I tell people you cannot count on your company and you cannot count on the government. The only thing you can rely on is yourself. So it’s really important to take control and start saving,” says Bill Losey, a retirement expert and certified financial planner in Greenwich, New York.

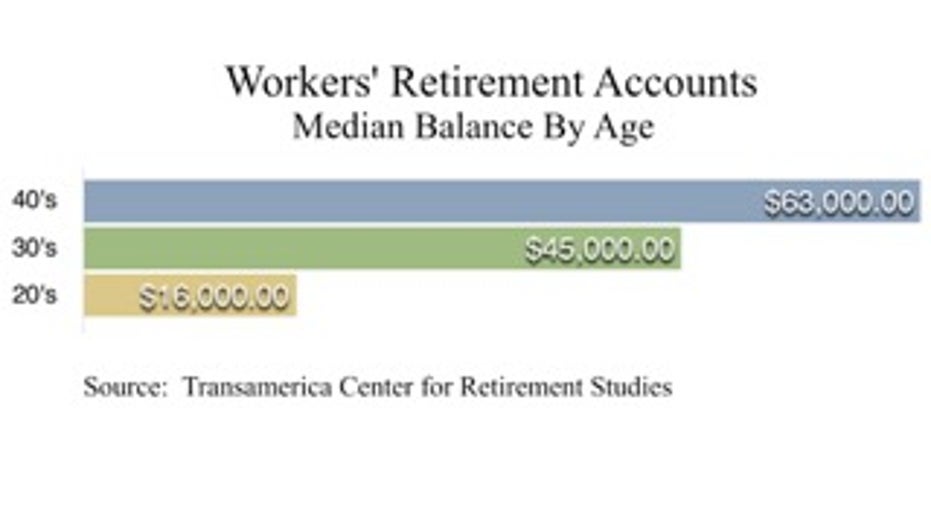

Many people will need well over $1 million in savings to keep their current lifestyle in retirement. Unfortunately, some people are not saving enough. One study found people in their 20’s had a median retirement savings of just $16,000. For people in their 30’s, that number was $45,000 and $63,000 for people in their 40’s. Many people also don’t start saving for retirement until well into their late 40’s when they need to think about other costs including college tuition.

Buying Too Much House

Many people fall for the American dream of having the white picket fence and the big, beautiful house. The dream house, however, probably comes at a hefty price. Americans are buying more expensive first homes with homebuyers spending about 60% more for a house compared to what first-time homebuyers paid in the 1970’s according to Zillow.

Financials advisers say homebuyers especially younger first-time homebuyers get lured into buying a house above their budget and fail to factor in additional costs. On top of a mortgage and property taxes, buyers also need to pay heating and maintenance costs as well as insurance and landscaping expenses. Add it all up and it could be a tremendous source of financial stress. Keep in mind, homebuyers also tend to downsize later in life.

The Solution: Consider a smaller home that fits in your budget. A general rule of thumb: don’t spend more than 30 percent of your monthly income on a mortgage. A smaller home also means lower utility costs, less cleaning and more money to save for yourself.

Not Paying Yourself First

Financial advisers say people especially when they are younger tend to pay everyone else except themselves. They work to pay the rent or mortgage, the car payment, the dry cleaning bill and the list of expenses goes on. Losey says it is important for young people to put themselves on that list and automatically set aside a portion of their salary to invest. “Time and compounding can really be your friend. Money will make money over time. Fresh out of school, start saving right away. If you save 10 percent of each paycheck, you could be a millionaire by the time you’re 40,” he says.

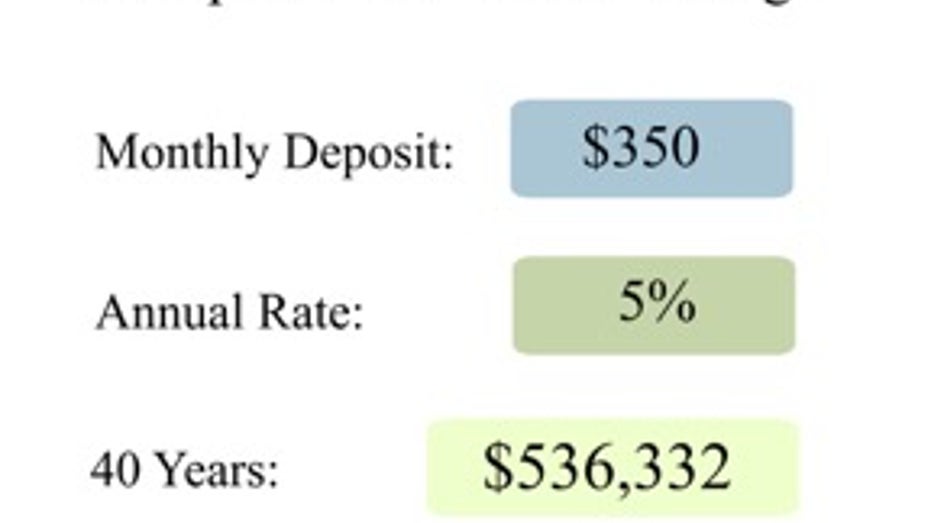

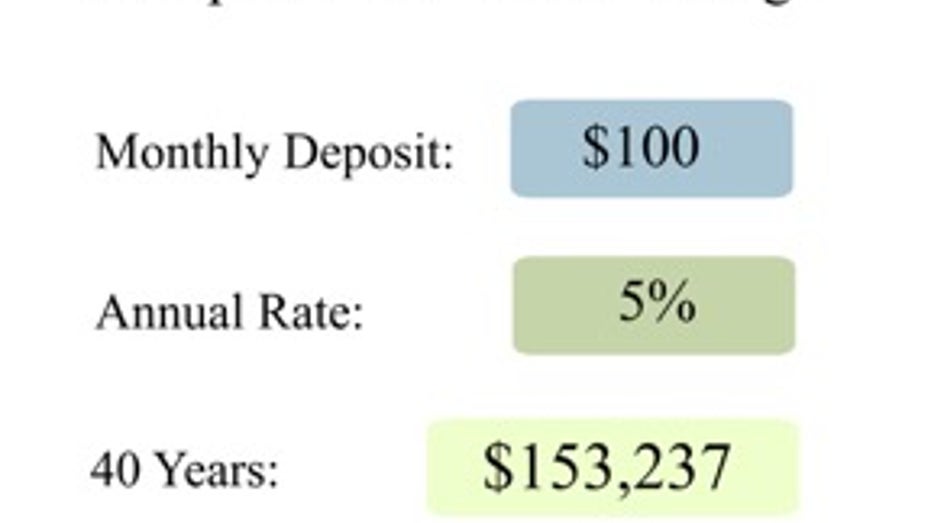

The Solution: Aim to set money aside for yourself automatically from your paycheck. It could payoff in a big way thanks to compounding. For example, by investing just a $100 a month with a 5 percent annual interest rate, you could be looking at more $153,000 in 40 years. Set aside $350 a month and you are looking at more than $536,000 in 40 years.

Overspending

Access to credit increases rapidly in your 20s and 30s. Young people tend to take advantage of that and overspend on fancy cars, exotic trips, expensive clothing and handbags. It is no surprise that data from the Federal Reserve also shows consumer debt tends to skyrocket in your 20s and 30s as credit becomes more available. Hefty credit card bills may also lead to high interest payments and one simple purchase could take years to pay off. If payments are late, there is also the risk of a lower credit score which could affect buying a home down the road.

The Solution: Financial adisers say it is important to establish a good credit history so opening a line of credit is not a bad thing. But there is no need to take advantage of every credit card offer you receive or max out your line of credit. The goal is to avoid overspending, pay your monthly bill in full and pay your bill on time. It may be tempting to treat yourself to a big purchase but if it is not in your budget, the consequences may be more negative than positive.